The Capital Crunch: Why Revenue-Based Financing Is the Answer to Today's Funding Gap

- Sage Growth Capital Team

- Apr 1

- 5 min read

As we analyze the landscape of startup funding in 2025, two comprehensive reports paint a stark picture: the SEC Office of the Advocate for Small Business Capital Formation Staff Report and Carta's State of Startups 2025. Together, they reveal critical gaps in capital availability for early-stage businesses; gaps that revenue-based financing is uniquely positioned to fill.

The Numbers Don't Lie: A Funding Crisis for Small Businesses

The data from the SEC's Office of Small Business Advocacy is sobering. In 2024, 94% of small businesses experienced financial challenges, with access to capital ranking as a top concern. When entrepreneurs did seek financing:

Only 43% received the total loan amount they requested

A mere 14% received all the venture capital they sought

Just 8% obtained the full grant funding they applied for

Only 7% successfully raised their complete crowdfunding target

Even more telling: 81% of small business owners who applied for a business loan or line of credit found it difficult to access affordable capital, with 40% seeking less than $50,000—relatively modest amounts that traditional lenders often overlook.

The VC Market: Longer Timelines, Higher Bars, Concentrated Capital

The venture capital landscape has fundamentally shifted. According to the reports:

Longer Time to Liquidity:

Companies are remaining private significantly longer; the number of companies staying private 8+ years after their first VC round has quadrupled from 2014 to 2024

45% of unicorns received their first VC funding round 9 or more years ago

The median time between financing rounds has increased to 2.1 years for Series D+ companies

In 2024, the median age of a company raising Series D+ reached 9.7 years

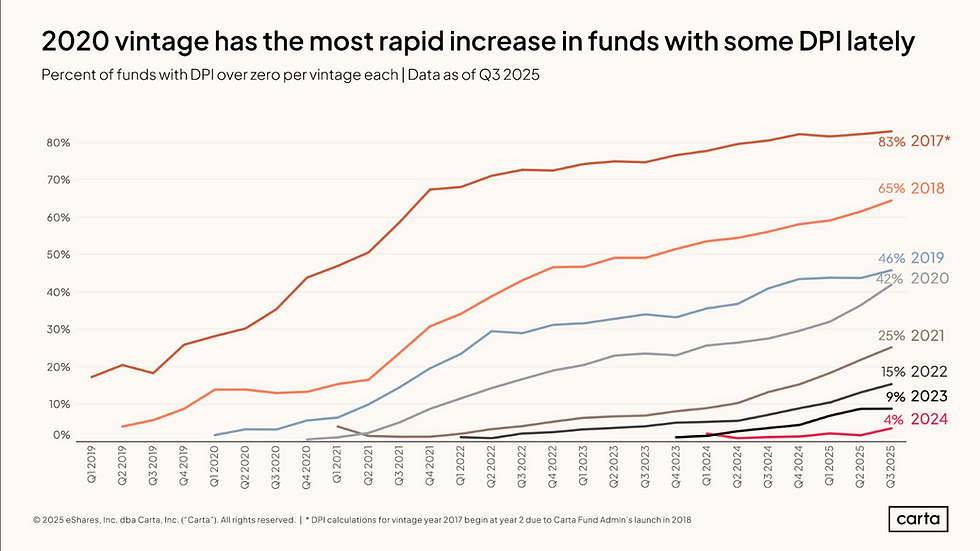

LPs are experiencing a liquidity crunch with distribution rates as low as 8-9% of net asset value (down from 34% in 2021)

Concentrated Capital:

In the first seven months of 2025, roughly 40% of all VC dollars went to just 10 companies

30 VC firms raised 75% of total VC dollars in 2024

The share of deals below $5 million fell to a decade low of 49% in H1 2025 (down from 72% in 2015)

18% of deals in H1 2025 were down rounds (compared to 8% in 2021)

Fundraising Challenges:

The average time spent fundraising increased to 17.4 months in H1 2025—the longest in over a decade

Fund managers raised 22% less capital in 2025 compared to previous years

For the first time in a decade, emerging managers closed fewer funds than experienced managers

Why This Matters: The Accessibility Gap

The reports reveal a critical insight: the pathways to capital that currently exist are failing the majority of entrepreneurs.

Consider these stark realities:

80% of early-stage businesses experienced macroeconomic challenges including uneven cash flow and difficulty accessing capital

64% of small business owners need technical assistance to access capital

11% didn't even apply for financing because they didn't know where to start

Meanwhile, the traditional VC model has become increasingly selective, focused on mega-rounds and later-stage investments:

VC investments have shifted from earlier stages to later-stage investments

Median deal sizes have grown substantially: Series A from $10M to $12M, Series B from $27M to $30M, Series C from $50M to $61M

Down rounds reached record high levels at 18% of deals, with 25% of Series D+ deals being down rounds

The Revenue-Based Financing Alternative

This is where revenue-based financing emerges as a critical solution. Unlike traditional VC, which demands:

Extended timelines (often 8-10+ years to exit)

Significant equity dilution: By Series A, founders collectively retain only 36% of their company (64% diluted). By Series B, just 23% remains (77% diluted). Each round typically dilutes founders by 18-20%, meaning founders who reach Series C often own less than 17% of the company they built.

Board seats and control

The pressure to achieve unicorn-scale outcomes

Revenue-based financing offers a fundamentally different value proposition:

Speed of Returns: Our fund structure has been delivering 50% DPI (Distributions to Paid-In capital) within 4 years and is on track to hit 100% within 5 years—a stark contrast to the decade-plus timelines now standard in VC. Both of our funds are on track to be fully liquidated at a profit within 7 years from closing each of them. For LPs experiencing the current liquidity crunch, this represents a breath of fresh air.

Accessibility: We serve the vast middle market of businesses that are:

Generating revenue but not yet profitable enough for traditional loans

Growing steadily but not at the hypergrowth pace VCs demand

Seeking $100K-$1M in capital

Building sustainable businesses, not necessarily unicorns

Alignment: Revenue-based financing aligns investor and founder incentives perfectly:

Payments scale with revenue (automatic flexibility during slower periods)

No equity dilution or board control

Founders retain ownership and decision-making authority

Success is measured by sustainable growth, not exit multiples

The Market Opportunity

The data shows a notable market gap:

Small businesses need capital: 94% face financial challenges, 40% seeking under $50K

Traditional pathways are failing: Only 7-43% get full funding across all channels

VC has moved upmarket: Median deals growing, early-stage share declining, concentration increasing

Liquidity is scarce: 8-9% distribution rates, 9.7-year median age for Series D+

Time to exit is extending: Companies staying private 8+ years, fundraising cycles lengthening

Revenue-based financing sits squarely in the middle of these trends:

Faster than VC (5-year DPI vs. 10+ years)

More accessible than traditional lending (revenue-based, not asset-based)

More flexible than venture debt (scales with revenue)

More founder-friendly than equity (no dilution or control)

The Case for LPs

For limited partners evaluating fund opportunities, revenue-based financing offers compelling advantages in today's environment:

1. Predictable Returns in an Uncertain Market

7-year fund life vs. 10-12+ years for traditional VC

Regular distributions starting within months, not years

100% DPI target within 5 years vs. 8-9% in early stage VC funds

2. Diversification Beyond Traditional VC

Access to high-quality companies outside the VC track

Revenue-generating businesses with proven models

Less susceptible to broader VC market cycles

3. Lower Risk Profile

Companies already generating revenue (not pre-revenue bets)

Downside protection through revenue-based payment structures

No binary outcomes (IPO or bust)

4. Alignment with Current Market Realities

Addresses the capital gap that both reports highlight

Serves the 49% of deals under $5M that VC is abandoning

Provides liquidity in an era of extended private company timelines

Looking Forward

The 2025 reports make it apparent that the traditional pathways for small business capital formation are under strain. Banks have consolidated (down 49% over the last decade), VC has moved upmarket and lengthened timelines dramatically, and entrepreneurs are left with fewer options than ever.

There's a massive gap in the market for flexible, founder-friendly capital that generates returns faster than traditional VC.

Revenue-based financing isn't trying to replace venture capital. It’s filling that gap for the thousands of businesses that are:

Already generating revenue

Growing sustainably

Seeking $100K-$1M in capital

Building for long-term success rather than unicorn exits

Looking to avoid dilution and maintain control

With our fund's ability to deliver 100% DPI within 5 years, we're positioned to serve both entrepreneurs seeking smart capital and LPs seeking predictable returns in an increasingly unpredictable market.

Sources:

About Sage Growth Capital

Sage Growth Capital makes revenue-financed investments in companies at any stage who need growth capital. It is our mission to provide a more flexible funding option to growing companies who do not fit traditional equity or lending models. To learn more about Sage Growth Capital or to apply for funding visit: www.sagegrowthcapital.com.

About Revenue-Financed Capital

Revenue-financed capital (RFC), also referred to as royalty financing, revenue share or revenue-based financing (RBF), is a non-dilutive form of growth capital where investors receive a percentage of monthly revenues until a set amount has been paid. RFC differs from equity financing as the investor does not obtain ownership of the company and it differs from debt financing as there is no collateral required and payments are variable. RFC is designed to empower entrepreneurs to grow their businesses with non-dilutive capital that aligns with their sales cycles.